What Ethereum intends to provide is a blockchain with a built-in fully fledged Turing-complete programming language that can be used to create ‘contracts’ that can be used to encode arbitrary state transition functions.

Vitalik Buterin, Ethereum Whitepaper (2014)

7.1 Learning objectives

By the end of this chapter the reader should be able to:

Contrast the UTXO model with the account model as two representations of a record that changes over time, the event-log form versus the current-state form, and derive the consequences of each for replay protection and parallel validation.

Explain why the account nonce is a counter, not a proof-of-work nonce, and state precisely what problem it solves.

Explain gas as a metered-computation solution to the halting problem, and convert gas and gwei into ether costs.

Derive and simulate the EIP-1559 base-fee update rule, and read it as a discrete-time feedback controller analogous to the difficulty adjustment of Chapter 5.

State what EIP-4844 blobs price, and why that pricing is a data-availability problem rather than a computation problem.

Evaluate a ‘health records on Ethereum’ proposal against the constraint that on-chain data is public.

7.2 Orientation

We begin with a problem in the governance of research data. Consider a longitudinal cohort study intended to follow its participants for a decade or more. The consent each participant grants is anything but monolithic: a given variable may be used for one purpose and not another, a given specimen may be shared with one laboratory and not a second, a permission may expire on a stated date, and any of it may be withdrawn at any time. In a study whose data are handled by dozens of analysts across several institutions over many years, enforcing that consent correctly is a substantial administrative burden, and the characteristic failure is familiar: a permission is revoked in one system and never propagated to the others, or a data-use condition is honoured by a conscientious analyst and quietly overlooked by a hurried one. We should prefer, if we could arrange it, that the permission rules execute themselves, so that access is granted or refused by machinery rather than by each downstream analyst’s individual diligence.

The device that makes a rule execute itself, in a setting where no single custodian is trusted to run it faithfully, is the smart contract, and it is the principal subject of this chapter. The idea did not originate in public health; its historical setting is digital cash, and the question Ethereum was built to answer was first posed in those terms. Bitcoin’s ledger answers one narrow question, namely which unspent outputs exist and who may spend them, and that question has a compact and beautifully parallel representation, the UTXO set, which needs nothing more to support a payment system. Ethereum was designed to answer a broader question: given an arbitrary program and an arbitrary starting state, what is the state after applying an arbitrary sequence of transactions? A consent policy that enforces itself is one instance of such a program, and answering the general question in a decentralised, adversarial setting is what the remainder of this chapter develops.

The reader already holds the right frame. A blockchain that supports general computation is a replicated deterministic state machine: every validator applies the same transition function to the same starting state and must reach the same ending state, or consensus fails. That is a transition function in the Markov-chain sense we have used for years, except that the state space is astronomically large (every account balance and every contract’s storage, all at once) and the transition function is written by whoever deploys a contract. The engineering problem is making that computation both expressive and safe to run on a machine we do not control, and the solution, gas, is a pricing mechanism before it is anything else.

This chapter also introduces the first genuine feedback controller we shall simulate end to end, namely the base fee of EIP-1559, the standard adopted in 2021 under which the protocol itself computes the per-gas price and adjusts it block by block rather than leaving it to an open auction. It is a smaller and more transparent system than the mining difficulty adjustment of Chapter 5, and studying it here, with the earlier controller already in hand, makes the general pattern, an error signal driving a multiplicative update toward a set point, impossible to miss the next time it appears.

We proceed as follows. We begin by contrasting the UTXO and account representations of a ledger, a choice we shall recognise as the event-log versus current-state distinction already met in representing a longitudinal record. We then describe the EVM as the shared deterministic machine on which contracts run, and gas as the pricing mechanism that makes running untrusted code on that machine safe. With those pieces in hand we develop EIP-1559 as a feedback controller and simulate its transient response, return to the programmable-consent problem with which we opened and scope precisely what a contract can and cannot be trusted to hold, and close with the data-availability pricing of EIP-4844, a 2024 change that adds a cheap, short-lived form of bulk on-chain storage.

Before proceeding we fix the vocabulary on which the chapter depends, so that the reader need not carry these terms as mysteries. Each is given in plain form here and treated more fully, with its statistical reading, in the section or table that follows.

NoteThe vocabulary of this chapter

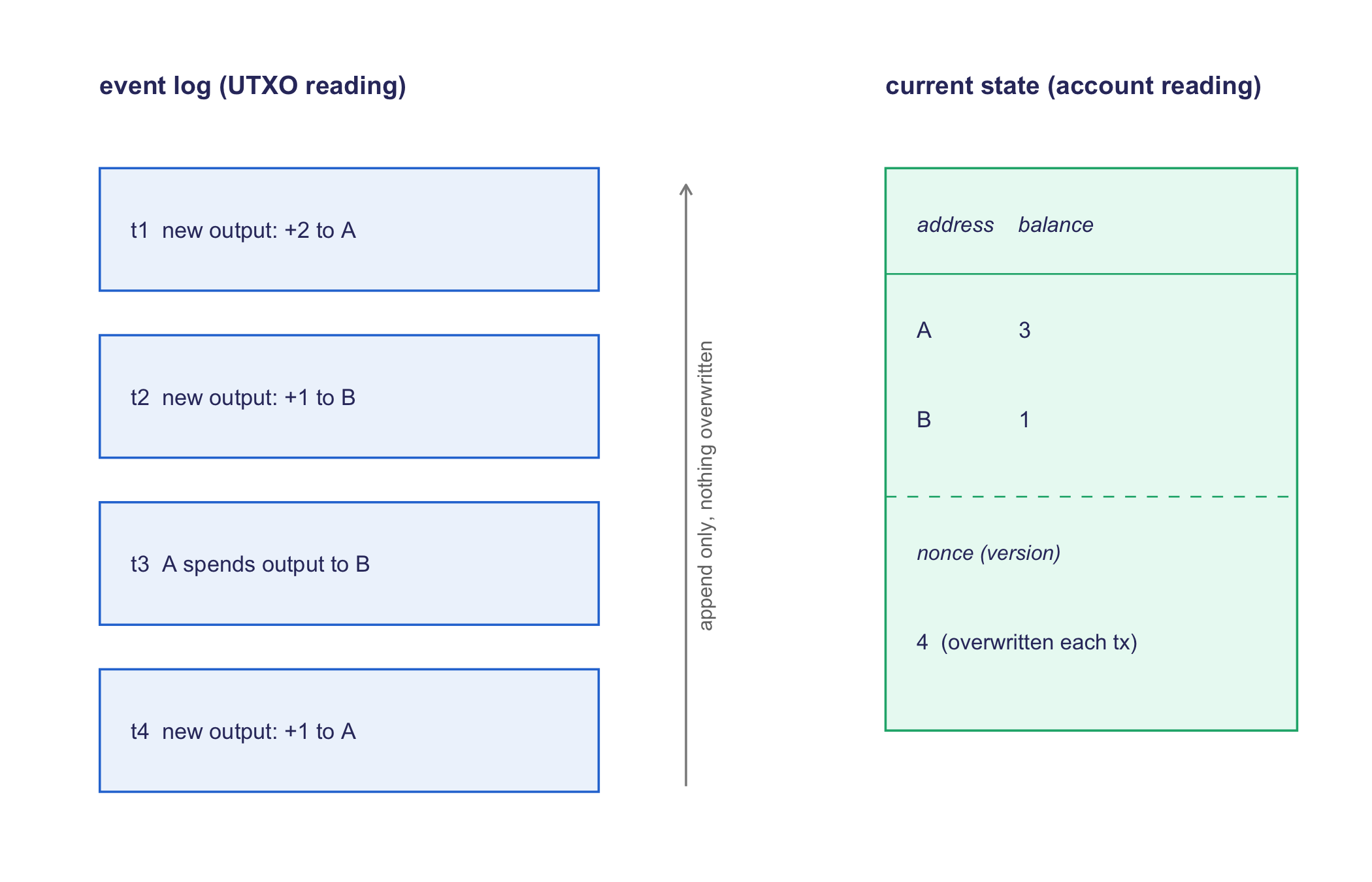

The UTXO and account models. Two ways a ledger may represent balances. In the UTXO (unspent-transaction-output) model, used by Bitcoin, the ledger stores discrete unspent outputs, and a balance is obtained by summing the ones an owner may still spend. In the account model, used by Ethereum, the ledger stores one running balance per address and overwrites it as transactions arrive.

Ethereum Virtual Machine (EVM). The shared, rule-bound computer that every Ethereum node runs identically, so that a given program applied to given inputs yields one and only one result on every machine.

Smart contract. A program stored on the ledger that runs automatically and identically on every node when it is called, enforcing its rules without any custodian trusted to execute them faithfully.

Gas and gwei. Gas is the unit in which the EVM meters computational work, each operation costing a fixed amount. Gwei is the small unit of ether, \(10^{-9}\) ether, in which the price paid per unit of gas is quoted.

Account nonce. A per-account counter, advanced by one with each transaction the account sends, that orders that account’s transactions and prevents a signed transaction from being replayed. It is unrelated to the mining nonce of proof-of-work met in Chapter 4.

Externally owned and contract accounts. An externally owned account is controlled by a private key held by a person or institution and may originate a transaction; a contract account is controlled by its own stored code and acts only when it is called.

7.3 The statistician’s contribution

Reading a fee market as a control system. EIP-1559 is not merely ‘a fee’; it is a proportional feedback loop with a known gain and a known set point. Recognising the update rule as a discrete-time controller lets us predict its transient behaviour under a demand shock and reason about stability, rather than treating the base fee as an opaque market outcome.

Recognising gas as a price on computational complexity. Gas costs are a per-opcode tariff schedule. Auditing a contract’s expected gas consumption is a complexity analysis in disguise, and the statistician’s habit of decomposing a total into per-unit costs applies directly.

Auditing determinism and its limits. The EVM is deterministic by specification, but a system ‘wired to’ the chain (an oracle feeding it a price, or a multisig, a wallet that requires several keys to authorise an action, holding an admin key) reintroduces trust and single points of failure that the deterministic core does not have. Distinguishing what the protocol guarantees from what a particular deployment adds is an exercise in scoping a claim correctly, which is exactly the discipline of Chapter 1’s falsifiability tiers.

7.4 From UTXO to the account model

We have already, in earlier chapters, met two ways of representing a record that changes over time. One may store the current state, a single row per entity that is overwritten as facts change, or one may store an event log, an append-only sequence of the changes themselves from which the current state is reconstructed by replay. The epidemiologist knows both forms intimately: a registry table holding each subject’s present status is a current-state representation, whereas a sequence of timestamped enrolment, visit, and outcome events is an event log. The contrast between Bitcoin’s UTXO model and Ethereum’s account model is precisely this data-modelling choice, transposed to a ledger, and the trade-offs are the ones the reader would anticipate. We set the two representations of the same ledger side by side in Figure 7.1 before drawing out their consequences.

library(ggplot2)library(tibble)PAL<-c('#2a78d6', '#1baf7a', '#eda100', '#008300','#4a3aa7', '#e34948', '#e87ba4', '#eb6834')book_theme<-ggplot2::theme_minimal(base_size =11)+ggplot2::theme( panel.grid.minor =ggplot2::element_blank(), panel.grid.major =ggplot2::element_line( linewidth =0.25, colour ='grey88'), axis.title =ggplot2::element_text(size =10), legend.position ='bottom')structure_col<-'#33356b'events<-tibble( y =c(6.0, 4.5, 3.0, 1.5), label =c('t1 new output: +2 to A','t2 new output: +1 to B','t3 A spends output to B','t4 new output: +1 to A'))ggplot()+geom_rect(data =events,aes(xmin =0.3, xmax =4.3, ymin =y-0.55, ymax =y+0.55), fill ='#eef4fc', colour =PAL[1], linewidth =0.4)+geom_text(data =events, aes(x =0.55, y =y, label =label), hjust =0, size =2.9, colour =structure_col)+annotate('text', x =0.3, y =7.3, hjust =0, label ='event log (UTXO reading)', fontface ='bold', size =3.3, colour =structure_col)+annotate('segment', x =5.0, xend =5.0, y =6.4, yend =1.0, arrow =arrow(length =unit(0.15, 'cm'), ends ='first'), colour ='grey55', linewidth =0.4)+annotate('text', x =5.15, y =3.7, hjust =0.5, angle =90, label ='append only, nothing overwritten', size =2.6, colour ='grey45')+annotate('text', x =6.6, y =7.3, hjust =0, label ='current state (account reading)', fontface ='bold', size =3.3, colour =structure_col)+geom_rect(aes(xmin =6.6, xmax =9.9, ymin =1.5, ymax =6.55), fill ='#eafaf3', colour =PAL[2], linewidth =0.4)+annotate('segment', x =6.6, xend =9.9, y =5.6, yend =5.6, colour =PAL[2], linewidth =0.3)+annotate('text', x =6.85, y =6.05, hjust =0, label ='address balance', fontface ='italic', size =2.8, colour =structure_col)+annotate('text', x =6.85, y =5.1, hjust =0, label ='A 3', size =2.9, colour =structure_col)+annotate('text', x =6.85, y =4.3, hjust =0, label ='B 1', size =2.9, colour =structure_col)+annotate('segment', x =6.6, xend =9.9, y =3.6, yend =3.6, colour =PAL[2], linewidth =0.3, linetype ='dashed')+annotate('text', x =6.85, y =3.1, hjust =0, label ='nonce (version)', fontface ='italic', size =2.7, colour =structure_col)+annotate('text', x =6.85, y =2.3, hjust =0, label ='4 (overwritten each tx)', size =2.8, colour =structure_col)+xlim(0, 10)+ylim(0.5, 7.7)+theme_void()

Figure 7.1: The same ledger under two representations. On the left the UTXO model keeps an append-only log of immutable outputs from which a balance is derived by replay; on the right the account model keeps one mutable row per address, plus a nonce that is overwritten as each transaction arrives.

To make the choice concrete, consider the running case study of this book, a data-integrity ledger for a multi-institution clinical trial in which several hospitals share a single append-only record of enrolment, randomisation, and outcome events, with no single trusted custodian and a regulator auditing after the fact. We shall refer to it as the trial ledger. The trial ledger is, by its nature, an event log: no hospital overwrites a prior entry, and the state of the trial at any moment (how many subjects are enrolled, to which arm each was randomised) is reconstructed by replaying the recorded events. Whether one then chooses to maintain a current-state summary alongside the log, and who is trusted to compute it, is precisely the UTXO-versus-account question in applied dress.

Bitcoin’s state is a set of unspent outputs, each locked by a script; a transaction consumes some outputs entirely and creates new ones. There is no notion of an account balance anywhere in the protocol: a balance is a client-side convenience computed by summing the outputs one can spend. This has two consequences worth stating precisely.

Replay protection is implicit. An output can be spent exactly once, because spending it removes it from the UTXO set; there is no separate counter to maintain, because consumption itself is the ordering mechanism.

Validation is embarrassingly parallel. Two transactions that spend disjoint sets of outputs touch disjoint state and can be validated concurrently; the only shared resource is the UTXO set membership test, which is a hash-table lookup.

Ethereum instead stores a mapping from account address to account state: a balance, a nonce, and (for a contract account) a code hash and a storage root. A transaction debits one account and credits another by directly mutating the balance fields, the way a bank’s ledger works, not the way a till full of physical banknotes works. In the vocabulary just introduced, the account model is a current-state representation: it stores each account’s present balance as a single mutable field and overwrites it as transactions arrive. The UTXO model, by contrast, is closer to an event log, in that the protocol stores the discrete outputs themselves and a balance is a derived quantity, reconstructed by summing the outputs an owner may still spend. The current-state form is the more natural representation for a programmable system, because a contract routinely needs to reason about the current balance of an address as a single persistent number (a token contract’s ledger, an escrow’s holdings) rather than reconstruct it from a history of discrete outputs every time.

The convenience of the current-state form is not free. The account model gives up the two UTXO advantages above and must manufacture substitutes.

Replay protection becomes explicit: the nonce. Because an account balance is a mutable field, two identical transactions (‘send 1 ETH from A to B’) are literally indistinguishable at the level of their content. Ethereum therefore attaches to every account a monotonically increasing counter, the account nonce, incremented by exactly one each time the account originates a transaction. A transaction is valid only if its declared nonce equals the sender account’s current nonce; once processed, the account’s nonce advances, so the identical transaction cannot be replayed, and transactions from one sender are strictly ordered by this counter.

WarningTwo different things named ‘nonce’

Do not conflate the account nonce with the proof-of-work mining nonce of Chapter 4. The mining nonce is a search variable in a discrete-uniform brute-force search over a hash’s range, re-chosen at random or by increment until a difficulty target is met; it exists per attempted block header and has no relationship to any specific account. The account nonce is a per-account counter with no cryptographic search attached to it at all; it exists to give a total order to one account’s transactions and to make replay of a signed message impossible. Ethereum uses the same English word for two unrelated objects, one from the consensus layer, one from the account layer, and the confusion this produces in casual writing is common enough to be worth naming explicitly.

Parallelisability is no longer free. Because two transactions from different accounts can still touch the same piece of shared state (both call the same contract, both trade against the same liquidity pool), validating and executing transactions in the account model cannot in general be parallelised without first inspecting which storage slots each transaction reads and writes. This is a genuine cost of the account model relative to UTXO’s disjoint-set structure, and it is one reason Bitcoin-style chains remain attractive for pure payment throughput even though they cannot express contracts.

Table 7.1 collects the contrast in one place, with the two consequences just derived, replay protection and parallelism, set beside the audit and use characteristics that follow from them.

Table 7.1: The UTXO and account models as event-log and current-state representations of the same ledger

Property

UTXO model (Bitcoin)

Account model (Ethereum)

State representation

Set of unspent outputs; balance is derived by replay

Mutable row per address (balance, nonce) overwritten in place

Replay protection

Implicit: spending removes the output

Explicit: per-account nonce counter

Parallel validation

Embarrassingly parallel over disjoint outputs

Not free: must inspect storage slots touched

Audit trail

Native event log of discrete outputs

Current-state snapshot; history reconstructed from blocks

Natural use

High-throughput payments

Programmable stateful contracts

NoteCheck your understanding: why not just hash the account state directly

Q. Why does Ethereum need an explicit nonce at all? Why not forbid resending a transaction whose exact byte content has already been seen, the way one might deduplicate by hashing?

A. Deduplicating by content hash prevents replay of the identical bytes, but it does not establish order. Suppose account A sends two different valid transactions in the same block, one to pay rent and one to buy groceries; both are distinct in content, so content-hash deduplication would accept either first. The chain still needs a rule for which one A intended to happen first, because A’s balance after the first affects whether the second is affordable. The nonce solves both problems at once: it forbids replay (nonce reused) and it fixes total order per sender (nonce 5 must be processed before nonce 6), which a content hash alone cannot express.

7.5 The EVM as a shared deterministic state machine

The Ethereum Virtual Machine is a stack-based virtual machine specified precisely enough that any two independent, correct implementations execute any transaction to bit-identical resulting state. That specification is Wood’s Ethereum Yellow Paper (Wood, 2014), the formal mathematical definition of the machine and of its state-transition rules. That determinism is the entire point: thousands of independently operated nodes must agree on the result of running arbitrary code without communicating during the computation, and they can only do so if ‘run this code on this input’ has exactly one possible answer.

Two kinds of accounts populate this state machine. An externally owned account (EOA) is controlled by a private key and has no code; it is the analogue of a Bitcoin address, the thing a human or an institution actually holds keys to. A contract account has code and, on receiving a transaction (or a message call from another contract), executes that code deterministically against its own persistent storage. Only an EOA can originate a transaction, meaning the chain always starts a state transition from a genuine act of key-holder authorization: this is the anchor that ties the ‘world computer’ picture back to the same signature scheme studied in Chapter 3. Table 7.2 sets the two account kinds side by side, read once more against the trial ledger, where a hospital holds an EOA and the shared record’s logic lives in a contract account.

Table 7.2: Externally owned accounts and contract accounts contrasted

Property

Externally owned account

Contract account

Controlled by

A private key

Its own deployed code

Can initiate a transaction

Yes

No; only reacts to a call

Holds code

No

Yes, executed deterministically

Trial-ledger reading

A hospital or auditor holding keys

The shared enrolment-logic and permission rules

Buterin, who proposed Ethereum in 2013, in the original Ethereum whitepaper (Buterin, 2014) describes this design as a single shared computer that anyone may submit programs to and whose entire history of execution is public and auditable. The framing is useful and also easy to over-read: it is one logical computer with thousands of redundant physical executions, which is why every unit of computation is expensive relative to a conventional server, a point the next section makes precise.

7.6 Gas as a solution to the halting problem

A Turing-complete language admits programs whose halting cannot be decided in general (the halting problem). A blockchain that executes arbitrary submitted code therefore faces a genuine hazard: a contract could contain a loop that never terminates, and every validating node would be obligated to run it forever, or forever fail to reach the state that depends on it. But how is a decentralised network to bound the cost of running code it did not write, without first solving a problem known to be undecidable?

Ethereum does not solve the halting problem. No one can. It sidesteps it economically: every EVM opcode, that is, every single primitive machine instruction, has a fixed gas cost, a sender must pre-purchase a gas limit for a transaction by paying up front, and execution halts the instant the gas supplied is exhausted, reverting all state changes made by that transaction (though the gas already consumed is not refunded). A transaction is therefore always guaranteed to terminate in bounded wall-clock time, because it is guaranteed to terminate in bounded opcode count, and opcode count times gas cost per opcode is bounded by the gas limit the sender agreed to pay for. This converts an undecidable question (‘will this program halt?’) into a decidable resource-accounting one (‘has this program consumed its budget?’), at the cost that some programs that would eventually halt on their own are killed early because their author underpriced them.

Gas is denominated in an abstract unit; what the sender actually pays is \[

\text{fee} = \text{gas used} \times \text{gas price},

\] where gas price is quoted in gwei, \(10^{-9}\) ether. A simple transfer costs 21{,}000 gas; a contract call can cost anywhere from tens of thousands to millions of gas depending on the storage writes and computation it performs (Antonopoulos & Wood, 2018). Because gas price is itself set by a market (studied next), the ether cost of the same computation varies with network demand even though the gas quantity for a given opcode sequence does not.

The vocabulary of the fee market is compact but easy to conflate, so we gather it in Table 7.3, each term paired with a statistical reading that recasts it as a familiar quantity: a per-unit cost, a price, a unit, a controller state variable, a premium, or a budget cap.

Table 7.3: A gas glossary, each term paired with its statistical reading

Term

Meaning

Statistical reading

Gas

Abstract unit metering work done by opcodes

Cost per instruction

Gas price

Ether paid per unit of gas

Price per unit

Gwei

\(10^{-9}\) ether, the unit gas price is quoted in

Unit of the price

Base fee

Protocol-set price per gas, burned

Controller state variable

Tip (priority fee)

Extra per-gas bid for ordering

Priority premium

Gas limit

Maximum gas a transaction may consume

Budget cap

NoteCheck your understanding: gas versus a CPU quota

Q. How does gas differ from an ordinary compute-time quota, such as a cloud function’s execution-time limit?

A. A time quota measures wall-clock seconds on one machine and is not portable across hardware of different speeds. Gas instead prices each EVM opcode individually, at a cost fixed by the protocol specification and independent of any single executor’s hardware. This is essential in a system where thousands of heterogeneous machines must all agree on exactly how much ‘work’ a given piece of code represents: the accounting has to be part of the protocol, not an artefact of whichever machine happens to run it, or nodes with faster hardware could disagree with slower ones about whether a transaction should have been killed.

7.7 EIP-1559: the fee market as a feedback controller

Prior to EIP-1559, Ethereum used a first-price auction for block space: senders bid a gas price, miners included the highest bidders, and the market cleared with high variance and a poor user experience, in that bidders routinely over- or under-paid relative to the true clearing price. EIP-1559 (Buterin et al., 2019) replaced this with a protocol-computed base fee that adjusts block by block toward a target utilisation, plus an optional priority fee (tip) that senders set to compete for ordering within a block. The base fee itself is burned, not paid to the block proposer, which is a monetary-policy design choice this chapter does not pursue further; the object of interest here is the update rule.

Each block has a gas limit and, since the London upgrade, a gas target set at half the gas limit. Let \(g_n\) be the gas used in block \(n\), let \(\bar g\) be the gas target, and let \(b_n\) be the base fee in force for block \(n\). The protocol sets

Read as a control system: \(g_n - \bar g\) is the error signal (how far the block’s gas usage deviated from the target), \(\bar g\) normalises it to a fraction, \(1/8\) is the proportional gain, and the update multiplies the previous base fee by \((1 + \text{gain} \times \text{error fraction})\). This is a discrete-time, first-order, multiplicative proportional controller: if blocks run consistently full (\(g_n > \bar g\)), the base fee rises geometrically each block until demand is priced out and usage falls back toward the target; if blocks run consistently empty, the base fee decays geometrically toward zero (in practice, toward a protocol floor). The controller has no integral or derivative term, so it corrects proportionally to the current error only, the same structural family as the Bitcoin difficulty adjustment of Chapter 5, which also multiplies the previous target by a ratio of observed to desired throughput. The two differ in what they control (a price, versus a proof-of-work difficulty) and in their update cadence (every block, versus every 2016 blocks), but the underlying idea, a set point, an observed deviation, and a bounded multiplicative correction, is identical, and recognising the pattern here is the payoff of having derived it once already.

For the reader whose intuition is clinical rather than industrial, an honest analogy from our own field is adaptive dose titration. In titrating a drug toward a target response, one raises the dose when the measured response falls short of the target and lowers it when the response overshoots, adjusting in bounded increments at each visit rather than leaping to a putative optimum. The base-fee rule has the same shape: the target utilisation plays the role of the target response, block fullness plays the role of the measured response, and the fixed 1/8 gain plays the role of the bounded per-visit dose step. We should be candid, however, about where the analogy ends, for it ends rather quickly. A titration protocol governs a single patient whose response follows a pharmacological process that is, at least in principle, stable and non-strategic; the base fee governs an aggregate of anonymous and frankly adversarial bidders who will reorganise their behaviour in anticipation of the rule itself. A clinician, moreover, may exercise judgment, impose safety bounds, and abandon a titration that is going wrong, whereas the base-fee controller is a fixed formula with no such discretion. The analogy is therefore useful for locating the base fee in a family of mechanisms the reader already understands, and misleading if pressed into a claim that a fee market will behave like a well-characterised dose-response curve.

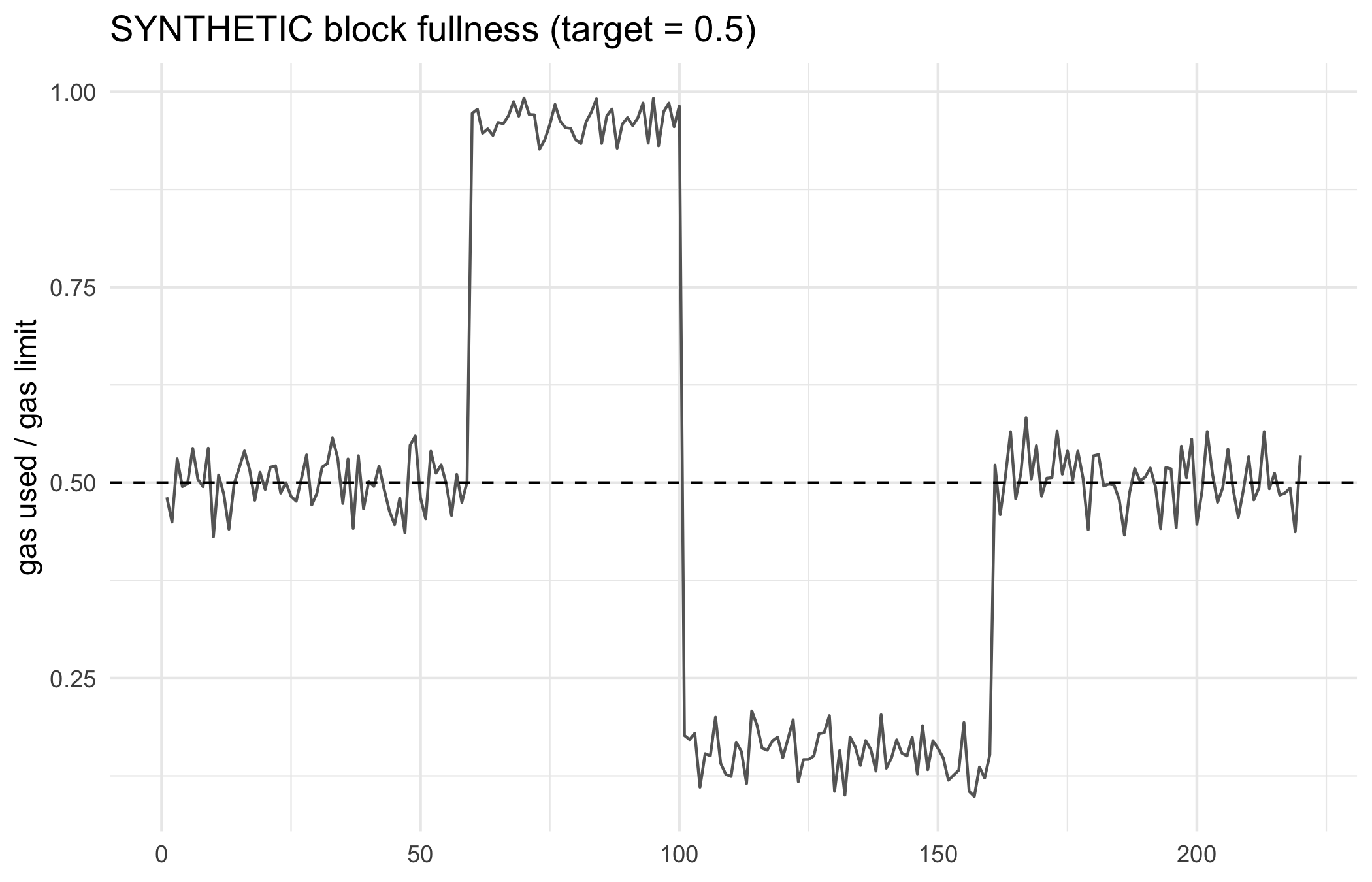

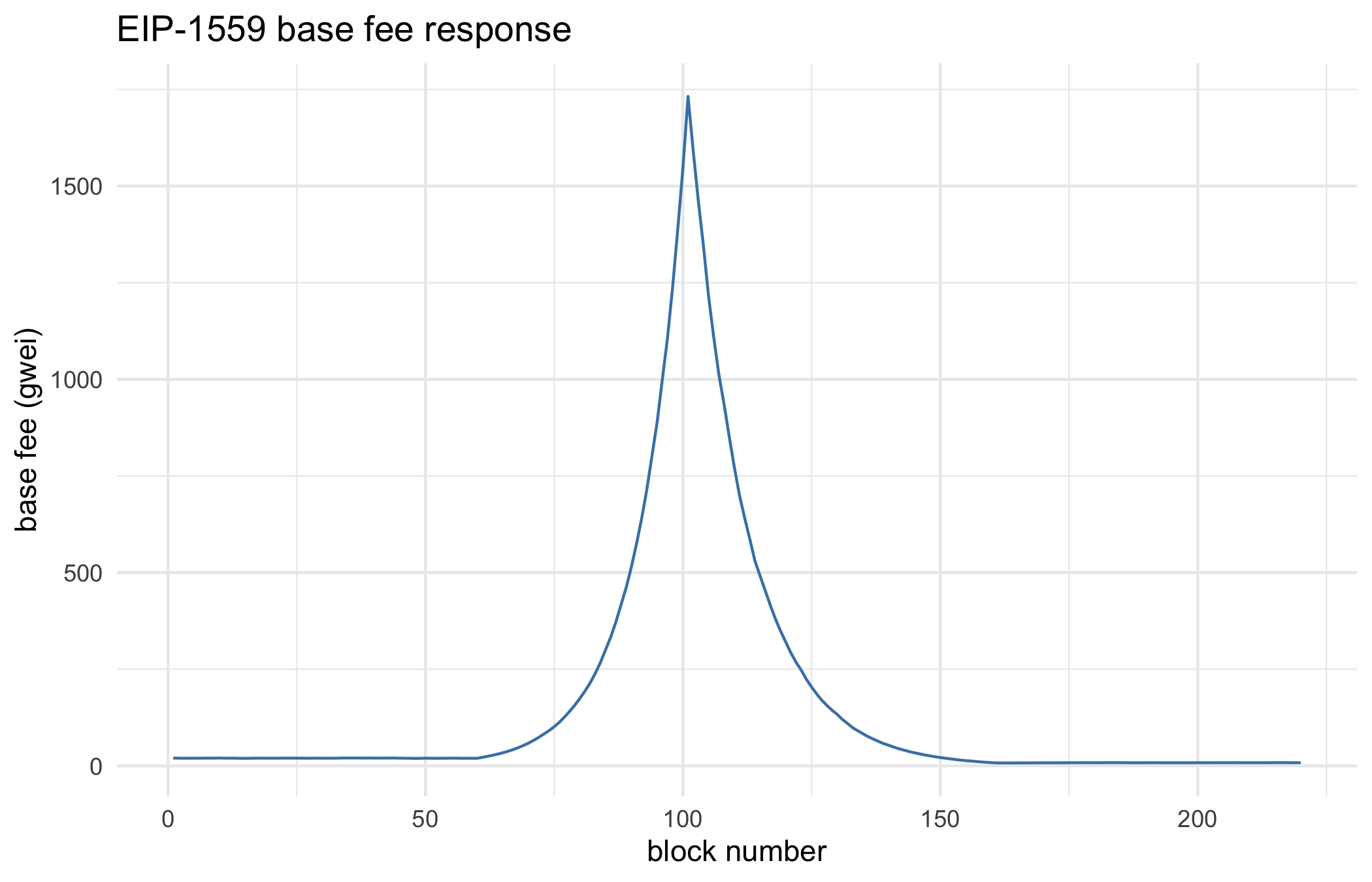

The following simulation is entirely synthetic: gas usage per block is not drawn from any real chain. It is constructed in three phases so that the controller’s full transient response is visible: a baseline near the target, a sustained demand shock that pushes blocks toward the gas limit, and a cooldown in which usage falls below target, the realistic consequence of a base fee that has become expensive enough to price out marginal demand, before the system settles back to a target-hugging baseline. A demand shock followed immediately by a return to exactly-target usage would leave the base fee permanently elevated with no force pulling it back down, because the controller only reacts to the current deviation from target; the cooldown phase is what actually drives the fee back down, and is a realistic feature of fee markets, not an artefact introduced for cosmetic effect.

library(ggplot2)library(dplyr)library(tibble)set.seed(20260703)gas_limit<-30e6gas_target<-gas_limit/2n_blocks<-220shock_start<-60shock_end<-100cooldown_end<-160# SYNTHETIC gas usage in three phases: near-target# noise, a sustained demand shock near the gas# limit, a cooldown below target (demand priced out# by the now-elevated fee), then a return to# near-target noise.baseline_frac<-rnorm(n_blocks, mean =0.5, sd =0.03)shock_frac<-rnorm(n_blocks, mean =0.97, sd =0.02)cooldown_frac<-rnorm(n_blocks, mean =0.15, sd =0.03)phase<-ifelse(seq_len(n_blocks)<shock_start, 'baseline',ifelse(seq_len(n_blocks)<=shock_end, 'shock',ifelse(seq_len(n_blocks)<=cooldown_end,'cooldown', 'recovery')))gas_used_frac<-pmin(pmax(case_when(phase=='shock'~shock_frac,phase=='cooldown'~cooldown_frac,TRUE~baseline_frac), 0), 1)gas_used<-gas_used_frac*gas_limit# base fee update rule, EIP-1559, applied# sequentially; base_fee[1] is an arbitrary starting# level in gwei.base_fee<-numeric(n_blocks)base_fee[1]<-20for(ninseq_len(n_blocks-1)){error_frac<-(gas_used[n]-gas_target)/gas_targetbase_fee[n+1]<-base_fee[n]*(1+error_frac/8)}sim<-tibble( block =seq_len(n_blocks), phase =phase, gas_used_frac =gas_used_frac, base_fee_gwei =base_fee)p_gas<-sim|>ggplot(aes(block, gas_used_frac))+geom_line(colour ='grey40')+geom_hline(yintercept =0.5, linetype ='dashed')+labs( x =NULL, y ='gas used / gas limit', title ='SYNTHETIC block fullness (target = 0.5)')+theme_minimal()p_fee<-sim|>ggplot(aes(block, base_fee_gwei))+geom_line(colour ='steelblue')+labs( x ='block number', y ='base fee (gwei)', title ='EIP-1559 base fee response')+theme_minimal()p_gasp_fee

Figure 7.2: SYNTHETIC gas usage across a demand shock and its cooldown (top) and the resulting EIP-1559 base fee path (bottom). The base fee rises geometrically while blocks run above target, then falls once the shock’s own expense pushes usage below target during the cooldown.

Figure 7.3: SYNTHETIC gas usage across a demand shock and its cooldown (top) and the resulting EIP-1559 base fee path (bottom). The base fee rises geometrically while blocks run above target, then falls once the shock’s own expense pushes usage below target during the cooldown.

The base fee is essentially flat while blocks hover near the 50 percent target, accelerates upward once the shock pushes usage toward the gas limit (each block above target compounds the previous block’s fee by up to 12.5 percent, the maximum single-block change under this rule), and then falls back once the cooldown phase pushes usage below target, settling near the end of the run below the pre-shock base fee: the controller has no memory of where it started, only of the current error, so the extended below-target cooldown pulls the fee past its original level before the final recovery phase holds it near target again. The 1/8 gain bounds the per-block change to at most \(\pm 12.5\%\), which is a deliberate design choice: it makes the fee predictable enough that a wallet can reliably compute ‘the base fee for the next block’ from public information (it is a formula, not an auction outcome), at the cost of responding to a genuine demand shock only gradually, block by block, rather than instantaneously.

ImportantThe sceptic’s reflex

‘EIP-1559 makes fees predictable’ is often stated as if it means fees became low or stable in level. It does neither. It is a tier-one protocol fact that the update rule is deterministic and computable from public information; it is a tier-three economic claim that this makes the ether cost of a transaction low or that base fee volatility disappeared. During a genuine demand shock the base fee still compounds geometrically block by block, and a user submitting a transaction still faces uncertainty about the tip required to be included promptly. What EIP-1559 actually delivers is a known functional form for the base fee’s evolution, which is valuable for wallets and for the statistician modelling the series, not a promise about its level.

7.8 EIP-4844: pricing data availability

EIP-4844 (Buterin et al., 2022) introduces blob-carrying transactions: a transaction type that attaches a large binary object (a ‘blob’, roughly 128 KB) which is stored by the consensus layer for a bounded retention window (currently on the order of eighteen days) rather than being kept permanently in state or processed by the EVM at all. Blobs are priced by their own independent EIP-1559-style mechanism, with their own target and limit per block, entirely separate from the gas market for ordinary execution.

The reason this needs its own market is that a blob is not purchasing computation, it is purchasing data availability: a rollup (a layer-2 chain that batches many transactions and periodically posts a compressed summary back to Ethereum) needs the underlying transaction data to be publicly available long enough for anyone to reconstruct and challenge the rollup’s state, but has no need for the EVM to execute anything against that data directly. Charging for this in ordinary gas conflated two different scarce resources, computation and storage-for-a- retention-window, that have different cost structures and different demand curves; EIP-4844 separates them into two independently clearing markets, each obeying the same controller family introduced above. This is best understood as the first concrete step of a broader scaling roadmap in which the base chain increasingly specialises in ordering and data availability, and execution moves to rollups; the details of that architecture are beyond this chapter’s scope, but the pricing logic is already in hand.

7.9 Scaling and the layer-two stack

To teach EIP-4844 and its blobs without first teaching rollups is to hand the reader an answer while withholding the question. Blobs exist because rollups need somewhere cheap to put their data, and rollups exist because the base chain, on its own, cannot carry the transaction volume that a general-purpose settlement layer is asked to bear. We take up that question here, and only with it in view does the data-availability pricing of the previous section acquire its motivation.

The difficulty is usually stated as a trilemma. A blockchain is asked to be decentralised (runnable by many independent, modestly resourced nodes), secure (costly to attack), and scalable (able to process many transactions per second), and the informal observation, which is engineering folklore rather than a theorem, is that a single base layer can comfortably supply any two of the three but not all three at once. The reason is already in hand from the account and EVM material of this chapter. Every full node re-executes every transaction against the shared state, because that is precisely what makes the result trustless: consensus holds only if each node can independently reach the same ending state. But how, then, is such a chain to process more transactions per second? Raising the throughput of a chain that every node must fully re-execute raises the hardware demand on every node in lockstep, and a chain that only a few well-resourced machines can keep up with has surrendered the decentralisation that motivated it in the first place. The re-execution that buys trustlessness is exactly what caps throughput.

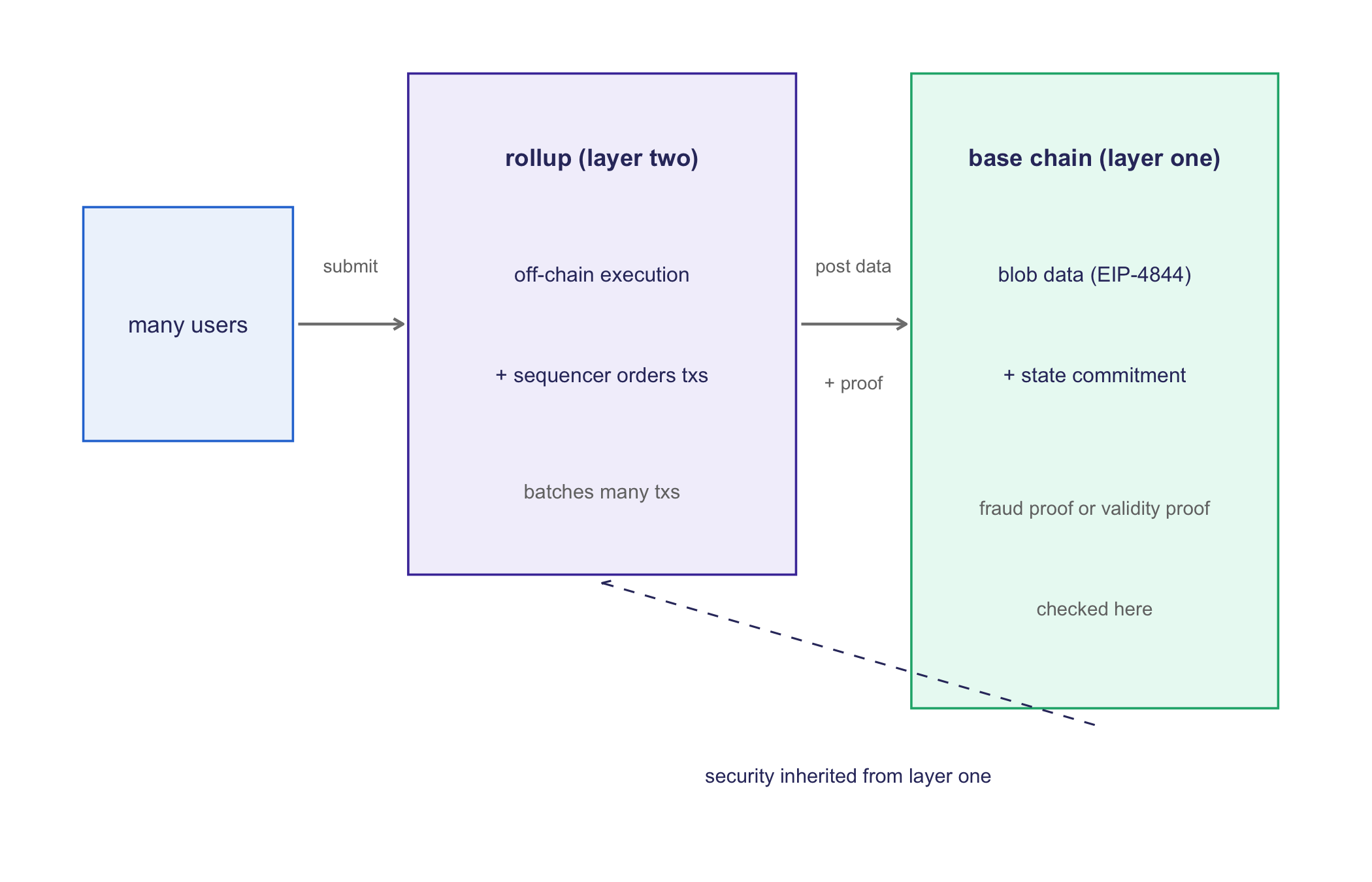

The dominant response, and the one the EIP-4844 material was quietly preparing, is to stop asking the base chain to execute everything. A rollup executes transactions off-chain, on a separate system with its own sequencer, the party that decides the order in which the incoming transactions are processed, and posts back to the base chain only a compressed record of what it did, together with enough information for anyone to check the result. Crucially, the rollup does not run its own consensus over who may write history; it borrows the base chain’s. Its data, or a proof of its correctness, is anchored on Ethereum, so that the security of the batched transactions reduces to the security of the layer they settle on. In the standard vocabulary the base chain is called layer one and the rollup built upon it layer two. The throughput gain comes from doing the expensive work, execution, once and off-chain, while the base chain is asked only to store the data and check a summary. We set the arrangement out in Figure 7.4.

library(ggplot2)PAL<-c('#2a78d6', '#1baf7a', '#eda100', '#008300','#4a3aa7', '#e34948', '#e87ba4', '#eb6834')structure_col<-'#33356b'box<-function(xmin, xmax, ymin, ymax, fill, col){annotate('rect', xmin =xmin, xmax =xmax, ymin =ymin, ymax =ymax, fill =fill, colour =col, linewidth =0.4)}ggplot()+box(0.2, 2.2, 5.0, 6.4, '#eef4fc', PAL[1])+annotate('text', x =1.2, y =5.7, label ='many users', size =3.0, colour =structure_col)+box(3.3, 7.0, 4.2, 7.2, '#f2f0fb', PAL[5])+annotate('text', x =5.15, y =6.7, label ='rollup (layer two)', fontface ='bold', size =3.1, colour =structure_col)+annotate('text', x =5.15, y =6.0, label ='off-chain execution', size =2.7, colour =structure_col)+annotate('text', x =5.15, y =5.4, label ='+ sequencer orders txs', size =2.7, colour =structure_col)+annotate('text', x =5.15, y =4.7, label ='batches many txs', size =2.6, colour ='grey45')+box(8.1, 11.6, 3.4, 7.2, '#eafaf3', PAL[2])+annotate('text', x =9.85, y =6.7, label ='base chain (layer one)', fontface ='bold', size =3.1, colour =structure_col)+annotate('text', x =9.85, y =6.0, label ='blob data (EIP-4844)', size =2.7, colour =structure_col)+annotate('text', x =9.85, y =5.4, label ='+ state commitment', size =2.7, colour =structure_col)+annotate('text', x =9.85, y =4.6, label ='fraud proof or validity proof', size =2.5, colour ='grey45')+annotate('text', x =9.85, y =4.0, label ='checked here', size =2.5, colour ='grey45')+annotate('segment', x =2.25, xend =3.25, y =5.7, yend =5.7, arrow =arrow(length =unit(0.14, 'cm')), colour ='grey50')+annotate('text', x =2.75, y =6.05, label ='submit', size =2.4, colour ='grey45')+annotate('segment', x =7.05, xend =8.05, y =5.7, yend =5.7, arrow =arrow(length =unit(0.14, 'cm')), colour ='grey50')+annotate('text', x =7.55, y =6.05, label ='post data', size =2.4, colour ='grey45')+annotate('text', x =7.55, y =5.35, label ='+ proof', size =2.4, colour ='grey45')+annotate('segment', x =9.85, xend =5.15, y =3.3, yend =4.15, arrow =arrow(length =unit(0.12, 'cm')), colour =structure_col, linetype ='dashed', linewidth =0.35)+annotate('text', x =7.5, y =3.0, label ='security inherited from layer one', size =2.6, colour =structure_col)+xlim(0, 11.9)+ylim(2.6, 7.4)+theme_void()

Figure 7.4: A rollup executes transactions off-chain and posts compressed data plus a state commitment back to the base chain, so that data availability and settlement are inherited from layer one while execution is not.

How the summary is checked divides rollups into two families, and the distinction merits precise statement, because it is a distinction in trust assumption and not merely in engineering. An OPTIMISTIC rollup posts its transaction data and simply asserts that the resulting state is correct, without proof; the assertion is accepted by default, subject to a challenge window during which any honest party who has recomputed the batch may submit a fraud proof demonstrating an invalid transition and reverse the result. Arbitrum (Kalodner et al., 2018), one of the most widely used optimistic rollups in production, is the canonical instance of this design. Its security rests on the assumption that at least one honest and attentive verifier exists and will act within the window, and on the underlying data being available for that verifier to check, which is exactly why blobs (Buterin et al., 2022) matter: the fraud proof is possible only if the data was published in the first place. A VALIDITY rollup, commonly a zero-knowledge rollup (one whose proof establishes that the computation was performed correctly while disclosing nothing about its inputs), instead posts a succinct cryptographic proof that the state transition was computed correctly, which the base chain verifies directly; there is no challenge window and no honest-verifier assumption, because an invalid batch cannot produce a valid proof. The proof machinery this relies upon is the zero-knowledge material we shall take up in Chapter 3, and we defer its mechanics to that discussion. Gudgeon et al. (Gudgeon et al., 2020) offer a systematisation of knowledge across the whole layer-two design space, and the reader who wishes to place these two families in their full taxonomy is referred to it. We set the two side by side in Table 7.4.

Table 7.4: Optimistic and validity rollups contrasted

Property

Optimistic rollup

Validity (zero-knowledge) rollup

What is posted

Transaction data plus an asserted new state

Transaction data plus a succinct validity proof

How correctness is enforced

Fraud proof during a challenge window

Cryptographic proof verified on-chain immediately

Trust assumption

At least one honest, attentive verifier acts in time

Rollups are not the only route off the base layer. The older idea is the payment or state channel, in which two parties (or a small group) open a channel by committing funds on-chain, then transact between themselves off-chain by exchanging signed balance updates, and settle back on-chain only when they close the channel; the intervening transactions, possibly very many of them, never touch the base layer at all. The Lightning Network (Poon & Dryja, 2016) is the best-known realisation of this idea, layered on Bitcoin, and it routes payments across a mesh of such channels so that two parties without a direct channel may still transact through intermediaries. Channels excel at high-frequency payments between stable sets of counterparties and are correspondingly poor at one-off interactions with strangers, to whom one would not open a funded channel in the first place; rollups, by contrast, serve open participation at the cost of the heavier machinery just described.

We should be candid about what layer two costs, for the throughput and the lower per-transaction fee are not obtained for nothing. Croman et al. (Croman et al., 2016), in an early and careful analysis of Bitcoin’s scaling limits, make the general point that scaling a decentralised ledger forces trade-offs rather than dissolving them, and the point transfers directly to layer two. On the one hand, a rollup genuinely raises throughput and lowers cost, by amortising execution over a batch and by paying only for data availability rather than for base-layer execution. On the other hand, it introduces trust assumptions the base layer did not carry: most rollups today run a single sequencer that orders transactions, and a centralised sequencer can censor or reorder, which is a weaker guarantee than the base chain’s; an optimistic rollup imposes a challenge-window latency, of the order of a week for withdrawals, during which a posted result is not yet final; and a validity rollup substitutes the considerable complexity of a proving system, whose own soundness must then be trusted. None of these is disqualifying, but each is a real cost, and a proposal that presents layer two as free throughput has simply not looked at the other side of the ledger.

The bearing on our own subject is direct. Consider a national-scale health-provenance system of the kind this book keeps returning to, one that records every vaccine vial and every custody transfer as it moves from manufacture to administration. The event volume such a system generates, tens or hundreds of millions of discrete provenance events, is far beyond what a base chain that every node re-executes could settle directly, and if one genuinely intends to operate at national scale, a rollup is the architecture by which the necessary throughput is reached. It is worth noticing that the sequencer-trust question this raises is not a new question at all. Whom do we trust to order and to publish the batched events, and what happens if that party misbehaves, is precisely the custodian question of Chapter 2 returning in a new guise, one layer up. The technology has moved the trust rather than abolished it, and locating exactly where it now sits is the whole of the analytic task.

We should be equally candid in the other direction. For the single-consortium trial ledger that has served as our running example, a handful of hospitals sharing one append-only record, the base layer’s throughput is already ample, and reaching for a rollup would add sequencer trust, proof-system complexity, or a challenge window in exchange for a throughput headroom the application does not need. The question of whether an added layer is warranted is a special case of the more basic question Wüst and Gervais (Wüst & Gervais, 2018) pose, namely whether one needs a blockchain at all; the discipline of asking it honestly does not stop at layer one. Layer two earns its complexity only when the transaction volume genuinely exceeds what the base layer can settle, and below that threshold it is complexity for its own sake.

NoteCheck your understanding: what does a rollup actually inherit

Q. A rollup is routinely described as inheriting the security of the base chain it settles on. Inheriting it in exactly what respect, and in what respect not?

A. It inherits data availability and settlement: once the rollup’s data and its commitment are posted to the base chain, they are as available and as immutable as any other base-chain data, and correctness is anchored on-chain by a fraud proof (optimistic) or a validity proof (zero-knowledge). What it does not inherit is censorship resistance in ordering. A single sequencer decides, off-chain, which transactions are included and in what order, and it can delay or exclude a user even though it cannot forge an invalid state transition. An optimistic rollup, moreover, does not inherit the base chain’s near-immediate finality, because a posted result is contestable until its challenge window closes. So ‘inherits security’ means the base chain guarantees that anyone can reconstruct and verify the rollup’s state, not that the sequencer cannot make a particular user wait.

7.10 When code is law: smart-contract security

The phrase most often used to commend the smart contract is that with it, code is law: the agreement executes itself exactly as written, and no clerk, no court, and no counterparty may intervene to alter the outcome. The determinism this chapter has emphasised is exactly what makes the promise credible. A contract does what its bytecode says and nothing else, every node agrees on the result, and no privileged party can quietly reinterpret the terms. What is said less often, and matters more, is the price of the same property. A contract executes exactly as written including where what was written is wrong, and on an immutable chain a discovered bug cannot be patched in place the way a flaw in a conventional service is corrected by deploying a fix. The code is law even when the code is mistaken, and the mistake is then as immutable as everything else on the chain.

The sharpest test this promise has faced is the attack on ‘The DAO’ in 2016. The DAO was a large investment fund encoded entirely as an Ethereum contract, holding what was at the time a substantial fraction of all circulating ether. An attacker discovered that its withdrawal logic was vulnerable to reentrancy and used the flaw to drain roughly a third of the fund before the community could react. The mechanism merits concrete statement, because it is both subtle and, once seen, unmistakable. Reentrancy arises when a contract makes an external call, handing control to another contract, before it has updated its own internal state to record the effect of that call. The DAO sent ether to the caller before decrementing the caller’s recorded balance; the receiving contract’s code, invoked automatically on receipt, simply called back into the withdrawal function again, and because the balance had not yet been reduced, the second call passed the same check and paid out a second time, and a third, looping until the funds were gone.

The response is what makes the episode the sharpest test ‘code is law’ has faced. If code truly is law, then the attacker merely executed the contract as written and was entitled to keep the proceeds. The Ethereum community, confronted with a loss of that magnitude, chose otherwise, and enacted a hard fork that rewrote the chain’s history to return the funds, a decision so contentious that a portion of the community rejected it and continued the original, unforked chain as Ethereum Classic, precisely on the principle that the code’s outcome, however unwelcome, ought to stand. That split is the standing reminder that ‘code is law’ is an aspiration held by fallible people, not a property the technology can guarantee on its own.

Reentrancy is only one of a family of vulnerability classes whose incidence is measurable rather than anecdotal. Atzei et al. (Atzei et al., 2017) provide a systematic survey of attacks on Ethereum contracts, organising them into recurring categories, and Luu et al. (Luu et al., 2016), with the Oyente analysis tool, showed that a large fraction of then-deployed contracts were flagged for at least one such class by automated symbolic analysis. The point for our purposes is not the precise percentages, which have shifted as tooling and language practice improved, but that these are structured, recurring, and to a considerable degree detectable defects rather than one-off misfortunes. Table 7.5 collects four of the most common classes with their mechanism and the standard mitigation.

Table 7.5: Four common smart-contract vulnerability classes

Vulnerability class

Mechanism

Standard mitigation

Reentrancy

An external call hands control to an untrusted contract before state is updated, letting the callee re-enter and repeat the operation

Update state before the external call (checks-effects-interactions), or use a reentrancy guard

Integer overflow/underflow

Arithmetic wraps past the fixed integer width, so a balance or counter silently jumps to a spurious value

Checked arithmetic (default in modern compilers) or a safe-math library

Access control

A privileged function omits or mis-scopes its authorisation check, letting any caller invoke it

Explicit caller checks on every privileged entry point, and least-privilege role design

Oracle manipulation

Logic depends on an external price or data feed an attacker can distort, for example via a flash-loan-driven price move

Time-weighted or multi-source feeds, sanity bounds, and treating any single oracle as untrusted

The bearing on the programmable-consent contract of this chapter is uncomfortable and merits facing squarely. That contract is exactly the kind of code whose bugs are irreversible. A consent contract that mishandles a revocation, that continues to adjudicate ‘allow’ after a participant has withdrawn permission because of an off-by-one in its logic or a reentrancy in its update path, has not committed a spreadsheet typo that a later correction quietly overwrites. It has recorded a permanent, on-chain error whose effects may already have propagated to every party that consulted it. This is a direct argument, from the security properties rather than from the privacy properties, for the same architecture the earlier public-health discussion reaches on other grounds: keep the on-chain logic minimal and auditable, and keep the sensitive data and the consequential decisions off-chain, where a mistake can be corrected before it becomes irreversible. The smaller the on-chain surface, the smaller the immutable attack surface.

ImportantThe sceptic’s reflex

‘The contract has been audited, so it is safe’ is the reassurance to distrust most. An audit is a finite inspection, by fallible reviewers, of a program whose behaviour is in general undecidable; it can establish the presence of the bugs it finds and never the absence of the bugs it does not. The DAO’s code had been read by many capable people before it was drained. Automated tools such as Oyente (Luu et al., 2016) raise the floor by flagging known classes mechanically, and they merit running, but a clean report is evidence of the absence of those particular classes, not a proof of correctness. We should treat ‘audited’ as a tier-two claim about what a reviewer looked for and did not find, never as a tier-one guarantee that the code is safe, and we should scope the irreversible on-chain logic small enough that an audit has a chance of being complete.

7.11 Public health connection: programmable consent, precisely scoped

We return now to the cohort study with which we opened. The proposal there was that a smart contract might encode a consent policy directly, so that the rule ‘this variable may be released to this researcher if this condition holds’ is enforced by code rather than by a data-use agreement that depends on institutional follow-through. But how much of a consent arrangement can a contract safely be made to carry? The computational content of the proposal is genuine and useful. A contract can hold a permission state (who is authorised, under what condition, until when) and can enforce access rules against anything routed through it with the same determinism this chapter has emphasised throughout, thereby removing a class of administrative failure in which a revoked permission is not actually propagated to every system that ought to honour it. This is the self-executing rule the opening asked for, and to that extent the intuitive appeal of the proposal is warranted.

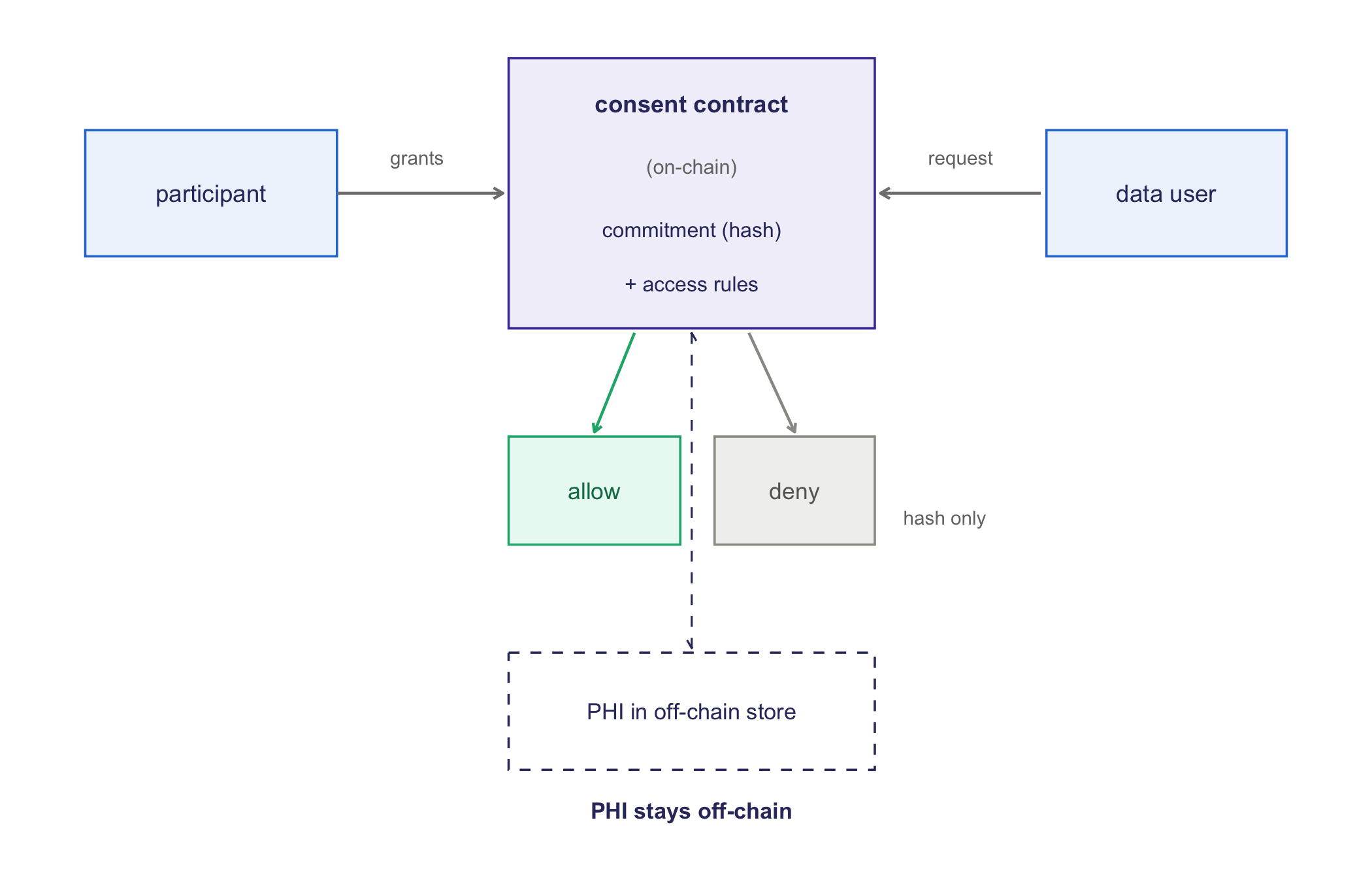

The proposal breaks, however, the moment it is extended to storing the protected health information itself on chain. Every full node holds a complete copy of chain state, in perpetuity, and no consensus mechanism studied in this book (nor any studied later) makes that state confidential; encryption of a field does not fix this, because the ciphertext persists forever and any weakness discovered in the encryption scheme, or any future key compromise, retroactively de-anonymises every record ever posted. A blockchain is therefore a defensible place to store a commitment to a permission (a hash of a consent document, an access-control state machine, a revocation flag) and an indefensible place to store the health data that permission governs. The correct architecture keeps PHI off-chain, in a system subject to ordinary access controls and regulatory obligations (HIPAA-equivalent controls, in a US setting), and puts on-chain only the tamper-evident metadata: who is permitted, since when, subject to what condition, and a hash committing to the off-chain record so that any party can verify a copy has not been altered without ever learning its content. Figure 7.5 draws the arrangement: the contract holds only a commitment and the access rules, adjudicates each request to allow or deny, and never touches the protected data, which stays in the off-chain store.

library(ggplot2)structure_col<-'#33356b'PAL<-c('#2a78d6', '#1baf7a', '#eda100', '#008300','#4a3aa7', '#e34948', '#e87ba4', '#eb6834')box<-function(xmin, xmax, ymin, ymax, fill, col){annotate('rect', xmin =xmin, xmax =xmax, ymin =ymin, ymax =ymax, fill =fill, colour =col, linewidth =0.4)}ggplot()+box(0.2, 2.4, 6.2, 7.6, '#eef4fc', PAL[1])+annotate('text', x =1.3, y =6.9, label ='participant', size =3.1, colour =structure_col)+box(3.9, 7.1, 5.4, 8.4, '#f2f0fb', PAL[5])+annotate('text', x =5.5, y =7.9, label ='consent contract', fontface ='bold', size =3.1, colour =structure_col)+annotate('text', x =5.5, y =7.2, label ='(on-chain)', size =2.6, colour ='grey45')+annotate('text', x =5.5, y =6.5, label ='commitment (hash)', size =2.7, colour =structure_col)+annotate('text', x =5.5, y =5.9, label ='+ access rules', size =2.7, colour =structure_col)+box(8.6, 10.7, 6.2, 7.6, '#eef4fc', PAL[1])+annotate('text', x =9.65, y =6.9, label ='data user', size =3.1, colour =structure_col)+annotate('segment', x =2.4, xend =3.85, y =6.9, yend =6.9, arrow =arrow(length =unit(0.14, 'cm')), colour ='grey50')+annotate('text', x =3.1, y =7.3, label ='grants', size =2.5, colour ='grey45')+annotate('segment', x =8.55, xend =7.15, y =6.9, yend =6.9, arrow =arrow(length =unit(0.14, 'cm')), colour ='grey50')+annotate('text', x =7.85, y =7.3, label ='request', size =2.5, colour ='grey45')+box(3.9, 5.4, 3.0, 4.2, '#eafaf3', PAL[2])+annotate('text', x =4.65, y =3.6, label ='allow', size =3.0, colour ='#0f7a52')+box(5.7, 7.1, 3.0, 4.2, '#f1f1ef', '#9a9a92')+annotate('text', x =6.4, y =3.6, label ='deny', size =3.0, colour ='grey40')+annotate('segment', x =5.0, xend =4.65, y =5.35, yend =4.25, arrow =arrow(length =unit(0.12, 'cm')), colour =PAL[2])+annotate('segment', x =6.0, xend =6.4, y =5.35, yend =4.25, arrow =arrow(length =unit(0.12, 'cm')), colour ='#9a9a92')+annotate('rect', xmin =3.9, xmax =7.1, ymin =0.5, ymax =1.8, fill ='white', colour =structure_col, linewidth =0.4, linetype ='dashed')+annotate('text', x =5.5, y =1.15, label ='PHI in off-chain store', size =2.9, colour =structure_col)+annotate('segment', x =5.5, xend =5.5, y =5.35, yend =1.85, arrow =arrow(length =unit(0.12, 'cm'), ends ='both'), colour =structure_col, linetype ='dashed', linewidth =0.35)+annotate('text', x =7.35, y =3.3, hjust =0, label ='hash only', size =2.5, colour ='grey45')+annotate('text', x =5.5, y =0.05, label ='PHI stays off-chain', fontface ='bold', size =2.9, colour =structure_col)+xlim(0, 10.9)+ylim(-0.3, 8.6)+theme_void()

Figure 7.5: Programmable consent, scoped correctly. The participant grants a permission whose commitment and rules live in an on-chain contract; a data user request is adjudicated allow or deny by that contract; and the protected health information itself stays in an off-chain store, with only a hash committed on chain.

To illustrate the commitment idea with something concrete, consider a single SYNTHETIC consent record, held in an off-chain store, of which we place on chain nothing but a cryptographic hash. The hash serves two purposes at once. It reveals nothing about the participant, since a good hash is not invertible, and yet it detects any later alteration of the off-chain record, because changing even one field changes the hash and the change no longer matches the value already committed. The following computes the commitment for an original record and for a silently widened one, in which a permission that named a single laboratory has been extended to a second.

library(digest)library(tibble)library(dplyr)# SYNTHETIC consent record. In a real deployment# this off-chain record lives in a HIPAA-governed# store; only the hash commitment goes on chain.consent<-tibble( participant_id ='SYNTHETIC-0007', permitted_use ='genomic-analysis', shared_with ='lab-B', expires ='2030-01-01', revoked =FALSE)commit<-function(record){digest(record, algo ='sha256')}original_hash<-commit(consent)# a single silent edit: the permission is widened# from one laboratory to two.tampered<-consent|>mutate(shared_with ='lab-B;lab-C')tampered_hash<-commit(tampered)tibble( version =c('original', 'tampered'), sha256_prefix =c(substr(original_hash, 1, 16),substr(tampered_hash, 1, 16)), matches_commitment =c(original_hash==original_hash,tampered_hash==original_hash))#> # A tibble: 2 × 3#> version sha256_prefix matches_commitment#> <chr> <chr> <lgl> #> 1 original 311bab12d9f59477 TRUE #> 2 tampered 23f3ee8ff0ee0e33 FALSE

The tampered record fails to match the on-chain commitment, so the alteration is detectable by any party holding the committed hash, and yet that hash, placed on a public and permanent ledger, discloses none of the participant’s information. This is the whole of what a blockchain contributes to the arrangement: tamper-evidence for a record whose contents remain elsewhere.

The secondary example the reader should keep in mind is vaccine cold-chain provenance. A distribution network would like an auditable guarantee that each vial remained within its permitted temperature range from manufacture to administration, across carriers and jurisdictions that do not fully trust one another. The structure of a defensible design is identical to the consent case: the sensor readings and custody transfers live off-chain, and the ledger holds only periodic hash commitments to them, so that a regulator can later verify that a presented temperature log has not been retrofitted to conceal an excursion, without the ledger itself becoming a public repository of the underlying operational data.

WarningMost ‘health records on Ethereum’ proposals fail this test

The reader should examine any concrete proposal for its precise placement of the boundary between what is committed on-chain and what is stored off-chain. A proposal that puts diagnosis codes, lab values, or free-text clinical notes on a public chain, encrypted or not, has misunderstood the guarantee a blockchain provides. The tier-one protocol fact is that on-chain state is public and permanent; a proposal that treats encryption as a substitute for that fact is making a tier-four narrative claim about future cryptographic durability, not a tier-one one about the system as built.

7.12 Worked example: base fee response to a rollup-driven demand shock

To illustrate, suppose gas usage on the base chain follows the SYNTHETIC pattern already simulated, and suppose we wish to quantify two things a network operator or an application developer genuinely cares about: how many blocks it takes the base fee to double from its pre-shock level, and how far it overshoots below the pre-shock level during the recovery. Both are directly readable from the simulated series already computed above.

Two features generalise beyond this particular synthetic run. First, doubling time is itself computable directly from the gain: a base fee that compounds by a constant fraction \(\epsilon\) per block for \(k\) blocks satisfies \(b_{n+k} = b_n(1+\epsilon)^k\), so if the shock holds usage at a constant fraction above target the doubling time is \(\log 2 / \log(1+\epsilon)\) blocks, which is a direct application of the compound-growth reasoning the reader already owns from continuous- time interest and population models, just discretised to one block per period. Second, the post-shock undershoot exists because the controller has no memory of the pre-shock level, only of the current error; a controller with an integral term would return exactly to a target level, and the base fee rule deliberately has none, trading long-run level stability for a simple, publicly computable per-block rule.

7.13 Collaborating with an LLM

Prompt: ‘Explain why Ethereum’s account model allows re-entrancy attacks and Bitcoin’s UTXO model does not.’ Watch for: a plausible-sounding answer that conflates re-entrancy (a contract-execution ordering bug, specific to stateful contract calls) with the account-versus-UTXO distinction itself; an LLM may imply the account model causes re-entrancy when in fact re-entrancy requires a contract that makes an external call before updating its own state, a coding pattern, not an unavoidable feature of the account model. Verification: ask for the specific EVM opcode sequence (a CALL before a storage write) that creates the vulnerability, and confirm against the Yellow Paper’s description of message calls (Wood, 2014) that re-entrancy is a consequence of contract code, not of the account-balance state representation per se.

Prompt: ‘Derive the maximum possible base fee after \(k\) consecutive full blocks under EIP-1559.’ Watch for: an LLM silently assuming the gain \(1/8\) acts additively rather than multiplicatively-compounding, giving a linear rather than a geometric bound. Verification: derive it yourself as \(b_0 (1 + 1/8)^k\) and check the LLM’s closed form reduces to the same expression; then check it numerically against the simulation code in this chapter by forcing gas_used_frac to 1 for \(k\) consecutive blocks.

Prompt: ‘Is it safe to store patient consent records on Ethereum?’ Watch for: an answer that treats ‘consent records’ as a single object and glosses over which fields are commitments versus which are the underlying protected data; this is exactly the tier-slippage the public-health section above warns against. Verification: insist the answer separately name, for each field of the proposed record, whether it is stored on-chain in plaintext, on-chain as a commitment (hash), or off-chain entirely, and reject any answer that does not make this partition explicit.

7.14 In conclusion

In conclusion, three points are to be emphasised. First, the account model is a current-state representation of a ledger, and the account nonce is the price of that choice: replay protection and a total order per sender, which the UTXO event log obtains for nothing, must in the account model be maintained explicitly, and the reader who keeps the event-log versus current-state distinction in view will not be surprised by where each cost falls. Second, gas and the EIP-1559 base fee are, respectively, a price on computation and a feedback controller on block utilisation; the base fee shares its structural family with the difficulty adjustment of Chapter 5, and it appears to us that recognising the controller pattern, a set point, an error signal, and a bounded multiplicative correction, is a more durable acquisition than any particular fee level. Third, and most consequentially for our own field, the defensible use of a blockchain in public health is to hold a tamper-evident commitment to a permission or a provenance record, and never the protected data itself; a proposal that places protected health information on chain, encrypted or otherwise, has misread the guarantee the technology provides, and the reader is now equipped to say precisely why.

7.15 Exercises

Derive the exact per-block bound on base fee change implied by the EIP-1559 update rule (that is, show the maximum possible ratio \(b_{n+1}/b_n\) and the minimum possible ratio, and state under what gas-usage condition each is attained).

Modify ch06-eip1559-sim so that instead of a single demand shock, gas usage follows a sinusoidal daily cycle around the target (SYNTHETIC data, your choice of amplitude and period in blocks). Plot the resulting base fee path and comment on whether the controller tracks a periodic input with a phase lag, and explain why a purely proportional controller cannot track a periodic input without lag.

A transaction’s total gas limit is 100{,}000 and the network base fee is 30 gwei with a 2 gwei priority fee. Compute the maximum ether cost of the transaction, and explain under what condition the sender pays strictly less than this maximum.

Explain, in terms of the account nonce, why a transaction with nonce 7 submitted before a pending transaction with nonce 6 from the same account cannot be included first, and contrast this with how Bitcoin would handle two transactions from the same address with no ordering dependency between them.

Using the falsifiability tiers of Chapter 1, classify each of the following claims and justify the tier: (a) ‘the EVM executes deterministically given identical inputs’; (b) ‘the average base fee fell after EIP-4844 shipped’; (c) ‘rollups will make on-chain health data storage economically viable’.

A contract’s admin key can pause the contract or redirect funds. Write two or three sentences evaluating the claim ‘this smart contract is trustless’ against that fact, using the sceptic’s reflex framework.

7.16 Further reading

Wood (2014) is the Ethereum Yellow Paper, the formal specification of the EVM and the account-state transition function; read it as the ground truth for every claim this chapter makes about determinism and gas accounting. Buterin (2014) is the original Ethereum whitepaper and is the right source for the ‘world computer’ framing and the motivating comparison with Bitcoin’s more limited scripting language. Buterin et al. (2019) is the EIP specifying the base-fee mechanism in full, including edge cases (block-limit elasticity, the initial base fee at the London upgrade) this chapter’s simulation abstracts away. Buterin et al. (2022) specifies blob transactions and the independent blob-gas market; read it alongside the main EIP-1559 specification to see how directly the second market reuses the first’s control law. Antonopoulos & Wood (2018) is the standard practitioner reference for account types, gas mechanics, and contract deployment, useful for the operational detail this chapter deliberately omits in favour of the underlying control-theoretic and economic structure. Narayanan et al. (2016) remains the standard comparison point for the UTXO model this chapter contrasts Ethereum against throughout.

Antonopoulos, A. M., & Wood, G. (2018). Mastering ethereum: Building smart contracts and DApps. O’Reilly Media.

Atzei, N., Bartoletti, M., & Cimoli, T. (2017). A survey of attacks on Ethereum smart contracts (SoK). Principles of Security and Trust (POST), LNCS, 10204, 164–186. https://doi.org/10.1007/978-3-662-54455-6_8

Buterin, V. (2014). A next-generation smart contract and decentralized application platform (ethereum whitepaper). Self-published. https://ethereum.org/en/whitepaper/

Buterin, V., Conner, E., Dudley, R., Slipper, M., Norden, I., & Bakhta, A. (2019). EIP-1559: Fee market change for ETH 1.0 chain. Ethereum Improvement Proposal. https://eips.ethereum.org/EIPS/eip-1559

Buterin, V., Feist, D., Loerakker, D., Kadianakis, G., Garnett, M., Taiwo, M., & Dietrichs, A. (2022). EIP-4844: Shard blob transactions. Ethereum Improvement Proposal. https://eips.ethereum.org/EIPS/eip-4844

Croman, K., Decker, C., Eyal, I., Gencer, A. E., Juels, A., Kosba, A., Miller, A., Saxena, P., Shi, E., Sirer, E. G., Song, D., & Wattenhofer, R. (2016). On scaling decentralized blockchains. Financial Cryptography Workshops (BITCOIN 2016), LNCS, 9604, 106–125. https://doi.org/10.1007/978-3-662-53357-4_8

Gudgeon, L., Moreno-Sanchez, P., Roos, S., McCorry, P., & Gervais, A. (2020). SoK: Layer-two blockchain protocols. Financial Cryptography and Data Security (FC 2020), LNCS, 12059, 201–226. https://doi.org/10.1007/978-3-030-51280-4_12

Luu, L., Chu, D.-H., Olickel, H., Saxena, P., & Hobor, A. (2016). Making smart contracts smarter. ACM SIGSAC Conference on Computer and Communications Security (CCS), 254–269. https://doi.org/10.1145/2976749.2978309

Narayanan, A., Bonneau, J., Felten, E. W., Miller, A., & Goldfeder, S. (2016). Bitcoin and cryptocurrency technologies: A comprehensive introduction. Princeton University Press. https://bitcoinbook.cs.princeton.edu/

Wüst, K., & Gervais, A. (2018). Do you need a blockchain? Crypto Valley Conference on Blockchain Technology (CVCBT), 45–54. https://doi.org/10.1109/CVCBT.2018.00011